In a life insurance company, especially an Islami life insurance or Takaful-based company, the most important financial strength indicators are:

- Life Fund

- Investment

- Claim Payment Ability

- Total Assets

These indicators determine the financial stability, solvency, credibility, and long-term sustainability of the company.

- Life Fund

Definition: A Life Fund is the accumulated fund created from policyholders’ premiums, investment income, and other insurance receipts, from which all policy benefits and claims are paid.

In Islami life insurance (Family Takaful), this fund is generally maintained separately as the Participants’ Fund or Policyholders’ Fund under Shariah principles.

Simple Meaning

It is the “policyholders’ money pool.”

All premiums go into the life fund, and all maturity claims, death claims, surrender values, bonuses, and benefits are paid from this fund.

Importance of Life Fund

The life fund is the most critical indicator of a life insurance company because:

- It shows the company’s financial strength.

- It determines whether the insurer can pay future claims.

- It reflects policyholders’ trust.

- A growing life fund means healthy business growth.

- Regulators evaluate solvency through the adequacy of the life fund.

If the life fund becomes weak or negative, the company faces difficulty in claim settlement and may become financially unstable.

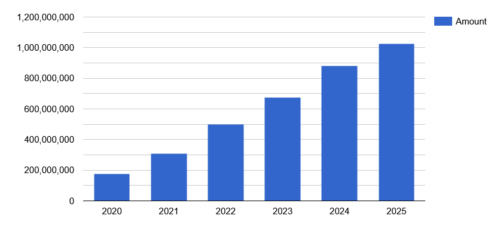

Five-year Life fund of Mercantile Islami Life Insurance Limited given bellow :

| Year | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 |

| Amount | 17,49,11,836 | 30,93,49,844 | 49,67,62,880 | 67,25,80,748 | 88,03,68,214 | 102,47,12,743 |

- Investment

Definition: Investment means the placement of life fund money into Shariah-compliant assets to generate profit and maintain liquidity for future claim payments.

Life insurers invest in:

- Government Sukuk/Bonds

- Islamic bank deposits

- Shares

- Real estate

- Corporate Sukuk

- Approved securities

Importance of Investment

Investment is the “engine of profitability” of a life insurance company.

Why It Is Important

- Generates profit for policyholders and shareholders

- Supports bonus declaration

- Strengthens life fund

- Ensures future claim payment ability

- Protects against inflation

- Improves solvency margin

Since life insurance is a long-term business, investment income is often a major source of profit.

Investment Allocation Process

The company determines investment based on:

- Size of life fund

- Future liabilities

- Liquidity requirements

- Shariah compliance

- Regulatory restrictions

- Risk and return balance

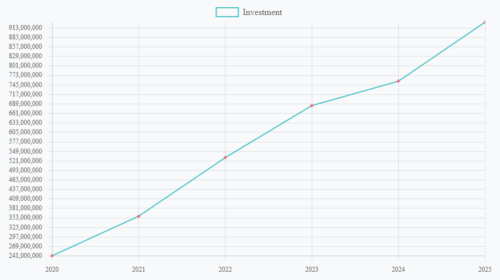

Five years Investment of Mercantile Islami Life Insurance Limited given below:

| Year | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|---|

| Amount | 24,10,26,650 | 35,78,85,713 | 53,06,65,2272 | 68,39,27,534 | 75,58,98,899 | 92,98,00,155 |

3. Claim Payment Ability

Definition: Claim payment ability means the financial capacity of the insurer to pay death claims, maturity claims, surrender claims, and other benefits on time.

This is the most important practical indicator from a policyholder’s perspective.

Importance

Strong claim payment ability means:

- High public confidence

- Strong liquidity position

- Positive reputation

- Regulatory compliance

- Business sustainability

Poor claim payment damages the company’s goodwill severely.

Recent reports in Bangladesh showed that weak life funds caused claim settlement crises in some insurers.

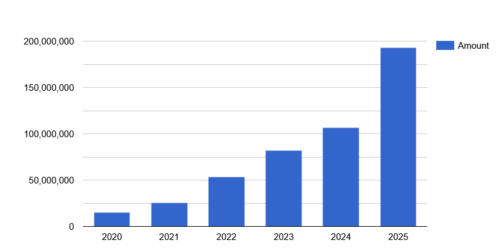

Five years Claim Payment of Mercantile Islami Life Insurance Limited given bellow :

| Year | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 |

| Amount | 1,48,83,464 | 2,52,20,661 | 5,35,56,496 | 8,16,45,908 | 10,64,70,465 | 19,26,28,562 |

- Total Assets

Definition: Total assets mean the total economic resources owned by the insurance company.

These include:

- Cash and bank balances

- Investments

- Property

- Receivables

- Premium dues

- Fixed assets

Importance

Total assets indicate:

- Overall company size

- Financial strength

- Market credibility

- Investment capability

- Solvency support

A large asset base increases confidence among:

- Policyholders

- Regulators

- Banks

- Investors

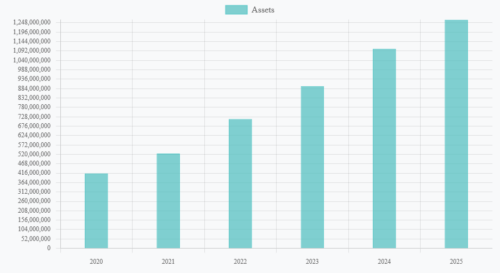

Five years Assets increment of Mercantile Islami Life Insurance Limited given bellow :

| Year | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 |

| Amount | 41,40,89,874 | 52,43,61,390 | 71,47,66,046 | 89,70,47,191 | 110,31,01,361 | 126,40,42,960 |

Relationship Among These Indicators

These four indicators are interconnected.

| Indicator | Effect |

| Higher Life Fund | Improves claim payment ability |

| Strong Investment Income | Increases life fund |

| Strong Claim Settlement | Builds customer trust |

| Larger Assets | Enhances solvency and stability |

Islami Life Insurance Perspective

In Islami life insurance (Takaful model):

- Investments must be Shariah-compliant.

- Interest-based investment is prohibited.

- Policyholders’ fund and shareholders’ fund are usually maintained separately.

- Risk sharing is emphasized instead of pure risk transfer.

Therefore, strong management of:

- Life fund,

- Halal investments,

- Liquidity,

- and claim settlement

is essential for maintaining public trust and Shariah compliance.

For a life insurance company, especially an Islami life insurance company, the core indicators of financial soundness are:

- Life Fund → Long-term policyholder security

- Investment → Profit generation and fund growth

- Claim Payment Ability → Customer confidence and liquidity strength

- Total Assets → Overall financial stability

A financially healthy life insurer generally has:

- Strong and growing life fund,

- Diversified halal investments,

- High claim settlement ratio,

- Strong asset base,

- Positive solvency margin,

- and sufficient liquidity for uninterrupted claim payment.